# 統計学実践ワークブック ####

# 第20章 分散分析と実験計画法 ####

# pp.167-172

# 参考

# https://www1.doshisha.ac.jp/~mjin/R/Chap_13/13.html

# [p.167]表20.1 ####

A1 <- c(9.7,8.7,10.2,11.3,11.2,11.7)

A2 <- c(9.8,11.8,13.1,10.9,11.3,10.3)

A3 <- c(9.2,10.0,10.2,8.9,10.4,10.6)

A4 <- c(13.1,12.6,12.7,12.6,14.3,12.9)

A5 <- c(10.8,10.5,13.0,11.9,13.4,10.3)

A <- rep(paste0('A',1:5), rep(6,5))

y <- c(A1,A2,A3,A4,A5)

df <- data.frame(A, y)

df |> head()

dev.off()

par(mfcol = c(1,1))

boxplot(y~A, data = df, col = "lightblue")

aov(y~A, data=df) |> summary()

# [p.170]表20.4 ####

A1 <- c(339,419,289,132,178,202)

A2 <- c(138,142,206,173,192,166)

A3 <- c(190,201,120,59,77,25)

A4 <- c(197,126,204,157,168,194)

A5 <- c(423,384,312,381,283,247)

A6 <- c(368,383,345,235,230,171)

A <- rep(paste0('A',1:6), rep(6,6))

B <- rep(paste0('B',1:2), rep(3,2))

y <- c(A1,A2,A3,A4,A5,A6)

df <- data.frame(A,B,y)

df |> head()

par(mfcol = c(1,2))

boxplot(y~A, data = df, col = "lightblue")

boxplot(y~B, data = df, col = "lightgreen")

aov(y~A*B, data=df) |> summary()

# [p.172]表20.6 ####

A1 <- c(5.2,12.3,7.1,20.5,9.4)

A2 <- c(3.8,11.3,7.2,18.5,9.0)

A3 <- c(7.2,15.3,10.6,25.3,11.1)

A4 <- c(3.5,10.2,8.5,20.2,10.7)

A <- rep(paste0('A',1:4),rep(5,4))

B <- rep(paste0('B',1:5),4)

y <- c(A1,A2,A3,A4)

df <- data.frame(A,B,y)

df |> head()

dev.off()

par(mfcol = c(1,1))

boxplot(y~A, data = df, col = "lightblue")

print("ブロック因子を導入した分散分析表の例")

aov(y~A+B, data=df) |> summary()

print("ブロック因子を導入しない場合の1元配置分散分析表の例")

aov(y~A, data=df) |> summary()

統計学実践ワークブック 第18章 質的回帰の問18.1-3のロジスティック回帰分析/プロビットモデルをRで実行

第18章 質的回帰

- データの引用元

- 統計学実践ワークブック pp.152-153

# 問18.1 #### # データ LIs <- c(8,10,12,14,16,18,20,22,24,26,28,32,34,38) Kanja <- c(2,2,3,3,3,1,3,2,1,1,1,1,1,3) Kankai <- c(0,0,0,0,0,1,2,1,0,1,1,0,1,2) # 加工 LI <- rep(LIs,Kanja) resp <- mapply( (\(x,y) c(rep(1,x),rep(0,y-x))), Kankai, Kanja ) |> unlist() df <- data.frame(LI,resp) # ロジスティック回帰 glm.logistic <- glm(df$resp ~ ., family=binomial(link="logit"), data = df) summary(glm.logistic) # [1]の確率 predict(glm.logistic, newdata = data.frame(LI=30), type = "response") # 問18.2 # データ Smokings <- c(0,1,0,1,0,1,0,1) Obesitys <- c(0,0,1,1,0,0,1,1) Snorings <- c(0,0,0,0,1,1,1,1) reisu <- c(60,17,8,2,187,85,51,23) kouketsus <- c(5,2,1,0,35,13,15,8) # 加工 smoking <- rep(Smokings, reisu) obesity <- rep(Obesitys, reisu) snoring <- rep(Snorings, reisu) resp <- mapply( (\(x,y) c(rep(1,x),rep(0,y-x))), kouketsus, reisu ) |> unlist() df2 <- data.frame(smoking,obesity,snoring,resp) # ロジスティック回帰 glm.logistic2 <- glm(resp ~., family = binomial(link = "logit"), data = df2) summary(glm.logistic2) # [1]の確率 predict(glm.logistic2, newdata = data.frame(smoking=1,obesity=1,snoring=1),type="response") # 問18.3 # プロビットモデル # データは問18.2と同じ glm.probit <- glm(resp ~., family = binomial(link = "probit"), data = df2) summary(glm.probit) # [1]の確率 predict(glm.probit, newdata = data.frame(smoking=1,obesity=1,snoring=1),type="response")

監査サンプリングについてのメモ

単語集

| 単語 | 意味 | 補足 |

|---|---|---|

| 監基報530 | 監査基準委員会報告書530 | 監査サンプリングについての記載がある。 |

| 逸脱 | 不備や例外を表していると思われる。 | |

| n | サンプルサイズ | 監基報530ではサンプル数と書かれている。 |

| k | サンプル内の逸脱件数 | |

| pT | 許容逸脱率 | 想定する母集団の逸脱率、ようするに母比率と思われる。TはTolerableの意味。 |

| pE | 予想逸脱率 | これがよく分からない。EはExpectedの意味。 |

| risk | 1 - 信頼度 | リスク |

確率として考える

は

- 逸脱なら

- そうでないなら

とする確率変数で、 は ベルヌーイ分布(

)に従っている。

すると、 は 二項分布(

) に従い、

さらに、 は二項分布(

) に従う。

となるような最小の は、逸脱件数:k とサンプルサイズ: n を用いて、

と表される。

統計として考える

Rでシミュレーションを実行するのと、二項分布の分布関数・分位点関数を用いて確認。

## 関数 AuditSim ####

# 母集団の大きさ: N

# 母集団に含まれる逸脱件数: K

# サンプルサイズ: n

# シミュレーション回数: how_many_times

## ####

AuditSim <- function(N=1000,K=50,n=45,how_many_times=10000){

paste("母集団の大きさ:",N,"\n") |> cat()

paste("母集団に含まれる逸脱件数:",K,"\n") |> cat()

paste("母集団の逸脱率:", K/N,"\n") |> cat()

paste("サンプルサイズ:", n,"\n") |> cat()

paste("シミュレーション回数:", how_many_times,"\n") |> cat()

cat("\n")

# 母集団設計 ################

# 母集団のサイズ: N

# 母集団に存在する逸脱件数: K

# 母集団作成

devi <- rep(1,K)

not_devi <- rep(0, N-K)

pop <- c(devi,not_devi)

# 標本設計 ################

# サンプルサイズ: n

# シミュレーション ################

# シミュレーション回数: how_many_times

# シミュレーション実行

replicate(how_many_times,{

# 母集団から無作為抽出でサンプルサイズnの標本を取得し

draws <- sample(pop, n, replace = TRUE)

# 標本の逸脱件数をカウントする

sum(draws)

}

) -> deviation_in_sample

# 結果確認 ################

# シミュレーションで得られた標本の逸脱件数の度数

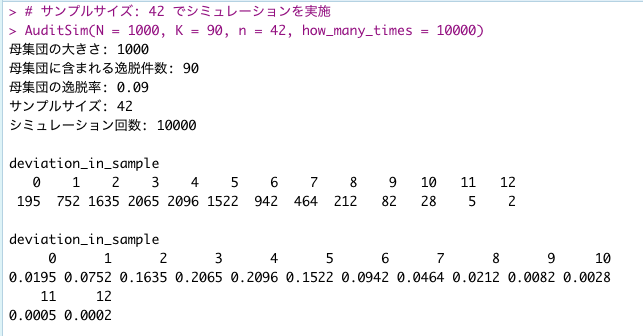

table(deviation_in_sample) |> print()

cat("\n")

# シミュレーションで得られた標本の逸脱件数の相対度数

(table(deviation_in_sample)/how_many_times) |> print()

cat("\n")# ヒストグラムの表示[標本の逸脱件数の度数]

hist_main = paste("Histogram of # of deviation in sample","\n","N=",N,"K=",K,"n=",n)

hist(deviation_in_sample, right = FALSE, main = hist_main, );box();}

# サンプルサイズ: 42 でシミュレーションを実施

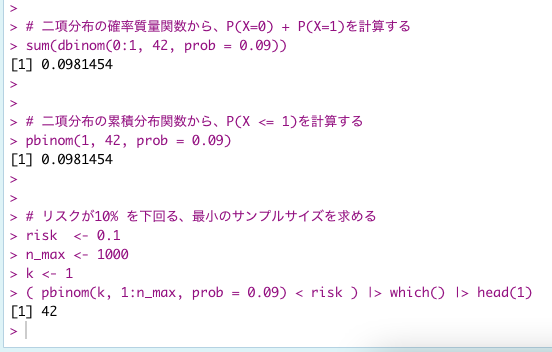

AuditSim(N = 1000, K = 90, n = 42, how_many_times = 10000)# 二項分布の確率質量関数から、P(X=0) + P(X=1)を計算する

sum(dbinom(0:1, 42, prob = 0.09))

# 二項分布の累積分布関数から、P(X <= 1)を計算する

pbinom(1, 42, prob = 0.09)

# リスクが10% を下回る、最小のサンプルサイズを求める

risk <- 0.1

n_max <- 1000

k <- 1

( pbinom(k, 1:n_max, prob = 0.09) < risk ) |> which() |> head(1)

実行例

資料集

清水公認会計士事務所 essays in some subjects: 統計

https://jicpa.or.jp/specialized_field/publication/files/2-24-530-2-20111114.pdf

2010 Attribute Sampling Plans

内部統制テスト・上限逸脱率の計算方法: Honeywar日記

https://www.saaj.or.jp/members/kaiho/201110SAAJKaihoNr128.pdf

内部統制は100回中8回間違えて良い - 内部統制ブログ(フジタヒロキ)

https://www.aicpa.org/publications/accountingauditing/keytopics/downloadabledocuments/sampling_guide_technical_notes.pdf

Workflow: Classical audit sampling • jfa

https://onlinelibrary.wiley.com/doi/pdf/10.1002/9781119448617.app1

「システム監査基準」及び「システム管理基準」の改訂について(METI/経済産業省)

https://www.ifac.org/system/files/downloads/translation_db_file_09.pdf

ガンマ関数とガンマ分布についてのポエム

統計学実践ワークブック第15章にて、"指数分布(λ)はガンマ分布(1, 1/λ)である"、というワンフレーズでつまずいたので、

復習を兼ねてポエムです。なお、以下の議論において、厳密性は度外視している。

ガンマ関数

定義

s > 0 とする。ガンマ関数Γ(s) は次式で定義される。

性質1: Γ(1) = 1

Γ(1) = 1である。

性質2: Γ(s) = (s-1)Γ(s-1)

Γ(s) = (s-1)Γ(s-1)である。

性質3: Γ(n) = (n-1)! where n ∈ ℕ

のとき、Γ(n) = (n-1)!である。

∵ 性質1と2より、ガンマ関数は

ガンマ分布

定義

a>0, b>0, x ∈(0,∞) として、確率密度関数f(x)が

と表される連続型確率分布を、ガンマ分布G(a, b) という。

モーメント母関数

X ~ G(a,b) としてモーメント母関数 を求める。

ここで とすると、

となる。

再生性

X ~ G(a1, b) , Y ~ G(a2, b) でXとYは互いに独立であるとする、この時 X+Yの分布はモーメント母関数を用いて

と表される。これは X+Y ~ G(a1+a2, b) に等しい。よってガンマ分布は再生性を持つ。

指数分布(λ)はガンマ分布(1, 1/λ)である

指数分布は確率密度関数が と表される。従って、ガンマ分布 G(a,b)にて

として求めると、

となり、確かに一致する。

マルコフ連鎖

統計学実践ワークブック問14.2より。

問題の概要

- 状態空間S = {1,2,3}

- マルコフ連鎖 X = (Xn)を以下に定める

- Xが状態iにあるとき、カードを1枚ランダムに引く。取り出したカードが

- a_i であれば状態iにとどまる

- a_j であれば

- 確率c_ij = min( j/i, 1 ) で状態jに推移

- 確率 1 - c_ij で iにとどまる

- Xが状態iにあるとき、カードを1枚ランダムに引く。取り出したカードが

- カードは復元抽出とする

- (1)マルコフ連鎖Xの確率推移行列Q を求めよ

問題の理解

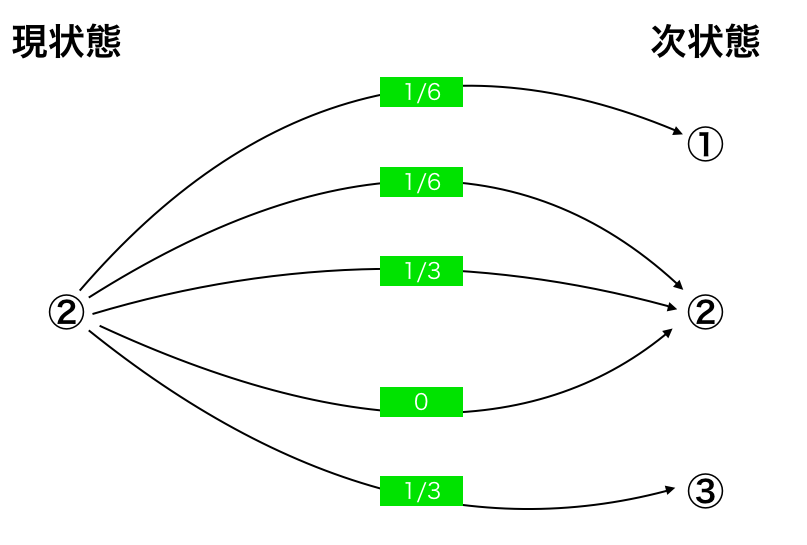

どのカードもどーよーにたしからしく引く、つまり1/3の確率で引くことができると考える。 また、各状態で「とどまる」とはつまり、状態iから状態iに推移すると言い換えることができる。

これらの点に注意しながら、以下「状態2」について詳細に計算過程を記述する。 なお、カードは[1][2][3]で表し、状態は①②③で表すとする。また、分数および1と0は確率のことを指している。

- ②のとき

- 1/3で[1]を引き当てる

- 1/2で①へ推移 ⇔ 確率1/6で ②→①と状態推移する

- 1/2で[2]へ推移 ⇔ 確率1/6で ②→②と状態推移する

- 1/3で[2]を引き当てる

- 1で②へ推移 ⇔ 確率1/3で②→②と状態推移する

- 1/3で[3]を引き当てる

- 1で③へ推移 ⇔ 確率1/3で②→③と状態推移する

- 0で②へ推移 ⇔ 確率0で②→②と状態推移する

- 1/3で[1]を引き当てる

これを状態推移ごとにまとめると、

| 状態推移 | 確率 |

|---|---|

| ②→① | 1/6 |

| ②→② | 1/6 |

| ②→② | 1/3 |

| ②→③ | 1/3 |

| ②→② | 0 |

となって、図で表現すると

となる。

従って、確率推移行列の第2行の成分は(1/6,1/2,1/3)となる。

同様に考えると、

- 第1行の成分は(1/3,1/3,1/3)

- 第3行の成分は(1/9,2/9,2/3)

となる。

切断正規分布

統計学実践ワークブックの問6.1〔4〕は、いわゆる切断正規分布の問題である。このキーワードでググると良い。

なお、期待値を求めるために確率変数 のモーメント母関数を計算しようとすると怪我をする?ので、素直に

から定義通り期待値を求めましょう。

2022-02-19 追記

ワークブックに従い、素直に確率密度関数f(z) = (1/2)×ϕ(z) where z > 0 , 0 where z ≦ 0 と考えた方が楽。